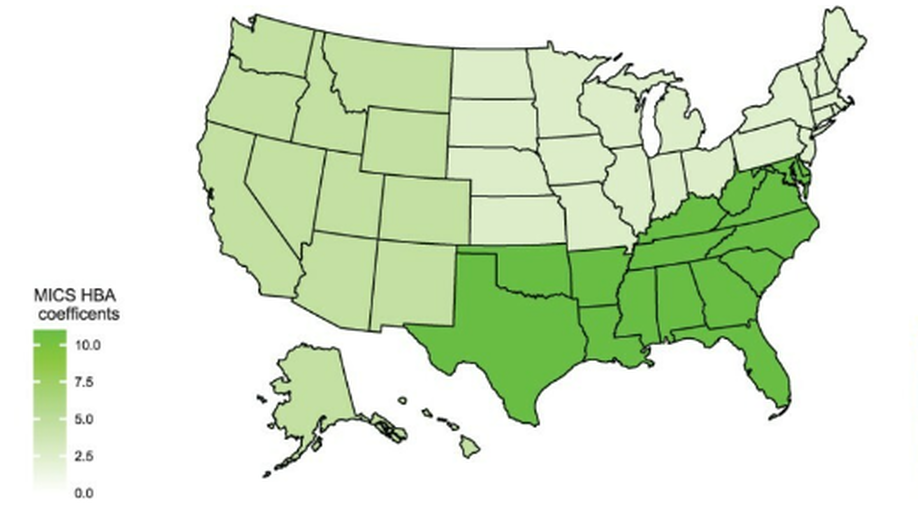

Investor sentiment’s effect on asset prices has been studied extensively to date, without delivering consistent results across samples and datasets. We investigate the asset-pricing impacts of eight widely cited investor-sentiment indicators (one direct, six indirect, one composite), within a unified long-horizon regression framework, predicting real NYSE-index returns over horizon lengths of 1, 3, 12, 24, 36, and 48 months. Results reveal that three of the non-composite indicators have consistent predictive power: the Michigan Index of Consumer Sentiment (MICS), IPO volume (NIPO), and the dividend premium (PDND). This finding has implications for the widely cited Baker-Wurgler first principal component (SFPC) composite indicator, which extracts information from the full set of six indirect indicators. As the diffusion-index literature shows, this type of wide-net approach is likely to impound idiosyncratic noise into the composite summary indicator, exacerbating forecasting errors. Therefore we create a new `targeted’ composite indicator from the first principal component of the three indicators that perform well in long-horizon regressions, i.e. MICS, NIPO, and PDND. The resulting targeted composite indicator outperforms SFPC in a market-returns prediction horse race. Whereas SFPC primarily predicts Equally Weighted Returns (EWR) rather than Value Weighted Returns (VWR), our new sentiment indicator performs better than SFPC in predicting both VWR and EWR. This improved performance is due in part to a reduction in overfitting, and in part to incorporation of the direct sentiment indicator MICS.